Spanish TravelTech Has Quietly Matured. Most Founders Are Still Solving the Wrong Problem.

What Spain's new tech census reveals about the Balearic Islands, the hotel industry, and the coming battle for data ownership.

A paradox in one number

Palma generates €45.6M in TravelTech revenue with just 8 companies. Barcelona generates €45.7M with 32.

Same revenue. Four times fewer companies.

This isn’t an anecdote. It’s arguably the most revealing data point in the new Tech & Innovative Companies Report 2025, a 319-page census of the Spanish tech ecosystem published by El Referente. And it’s a number almost no one is talking about.

It means the TravelTech ecosystem in the Balearic Islands has reached a level of efficiency and maturity that doesn’t exist in any other Spanish hub. And it raises an uncomfortable question for the industry as a whole: if the Balearics is proving you can scale TravelTech with brutally good economics, why is the rest of the sector stuck under an invisible ceiling?

The answer, I think, is more interesting than it looks.

The Spanish ecosystem has reached maturity

Some macro context first. The El Referente report is unambiguous: Spain is no longer an emerging tech ecosystem. It’s a mature one.

8,580 tech companies catalogued. 1,550 more than last year — 22% growth. €14.8 billion in annual economic impact. 108,000 jobs. 484 scaleups, with criteria significantly more restrictive than in previous editions (the report explicitly warns that the scaleup definition has been tightened and the data is not directly comparable to 2024).

This isn’t a fledgling sector. It’s a consolidated industry with its own gravity. Madrid concentrates 2,351 tech companies. Catalonia, 2,189. Valencia, 966. Below them, a long list of regional ecosystems with increasingly defined identities.

But behind the aggregate numbers, there’s a sectoral story that deserves a closer look.

Spanish TravelTech tells a different story

Spanish TravelTech has 174 companies today. They generate €762M in revenue and 3,201 jobs. By company count alone, the sector ranks 17th nationally — below Ehealth, Biotech, Edtech, and SaaS.

But that ranking is misleading.

Look at the sector’s actual maturity: 24 of those 174 companies are scaleups. That’s a concentration significantly higher than the Spanish tech average. This isn’t a small niche — it’s a small but heavily consolidated sector.

And then there’s the capital. In 2024, Spanish TravelTech attracted €454M in investment. In 2023, €46M. Nearly 10x in a single year. Smart money has decided something big is going to happen here — and it has positioned itself accordingly.

There’s capital. There’s maturity. The smart money is already in. And yet, of 92 Spanish TravelTech startups, only 24 have scaled. What about the other 68?

And the Balearic Islands tell the report’s most striking story

This is where the Balearics get interesting.

19 TravelTech companies operate in the islands. They generate €85.7M in revenue. That accounts for 36% of all tech revenue in the Balearic region — more than any other productive sector. In other words, in the Balearics, TravelTech isn’t just a sector. It is the sector.

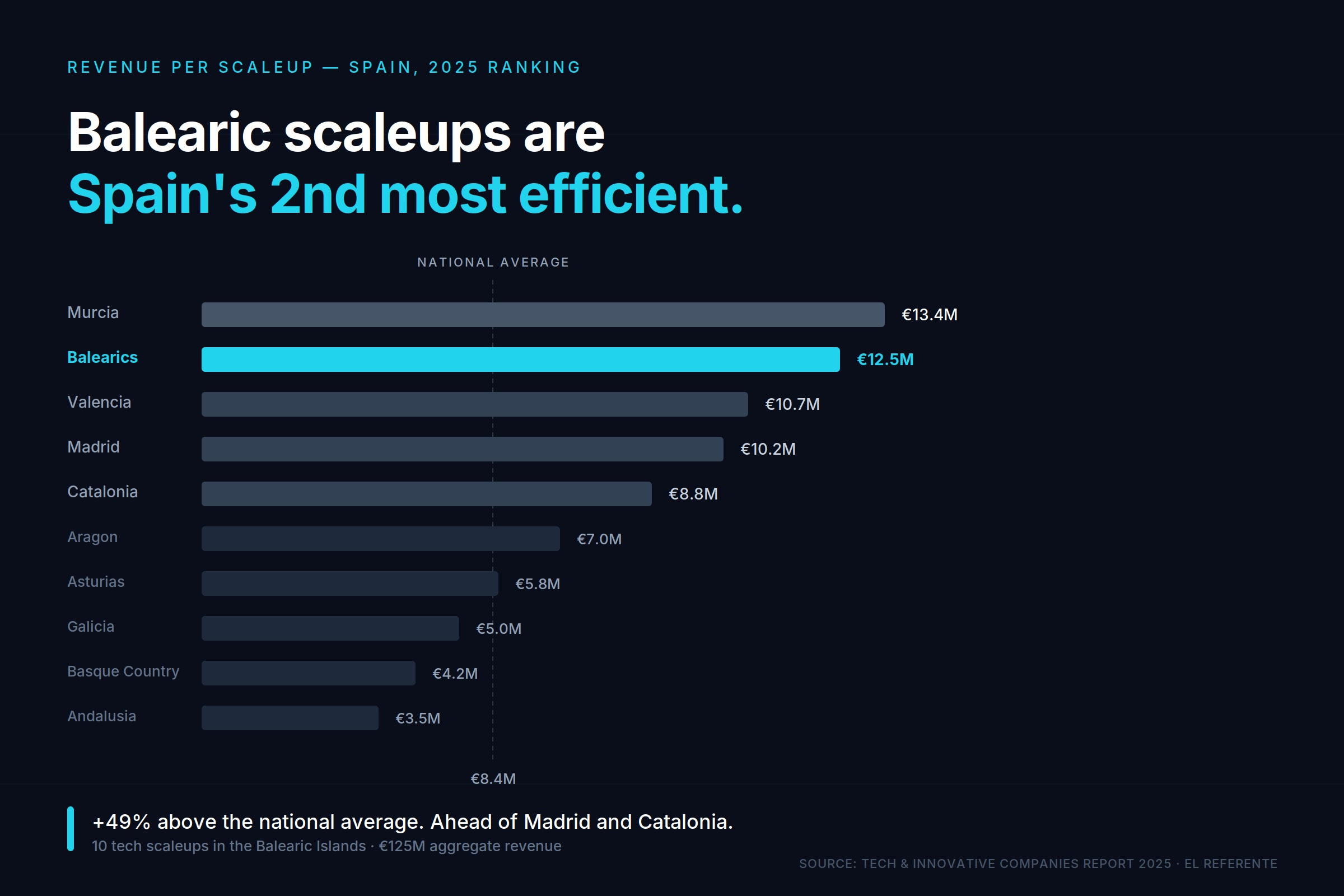

But the most revealing data point is something else. The 10 tech scaleups in the Balearic Islands (across all sectors) generate an average revenue of €12.5M per company. The Spanish national average is €8.4M. That places the Balearics as the second-most efficient Spanish region per scaleup, behind only Murcia (a statistical anomaly driven by a single outlier company). Ahead of Madrid (€10.2M per scaleup). Ahead of Catalonia (€8.8M). Far ahead of the Basque Country (€4.2M).

Add to that an investment number that has flown under the radar: in 2024, the Balearics closed 4 investment rounds worth €14.88M — almost the same amount as all Balearic tech investment accumulated over the previous eight years combined. Capital is now looking to the islands, and for the first time at meaningful scale.

And yet most companies don’t scale. Why?

This is the question the report doesn’t answer — but those of us inside the sector have been answering for years.

The short answer: most companies are solving the wrong problem.

We’ve been stuck in a feature war for fifteen years. Every year, dozens of TravelTech startups launch products that promise to “optimize hotel operations”: faster channel managers, prettier PMS interfaces, AI-driven revenue management modules, upsell tools, real-time guest feedback systems. Each tool solves a specific operational pain. And each tool is, fundamentally, irrelevant if it doesn’t solve the problem that actually matters.

Because the hotelier’s real problem isn’t operational. It’s structural.

Today, a huge share of bookings for independent hotels and mid-market chains comes through OTAs — Booking, Expedia, and their derivatives. OTAs charge between 15% and 25% commission per reservation. But the commission is just the tip of the iceberg. What they really take — and what’s worth fighting for — is the customer data.

When a guest books through Booking, Booking knows who they are, what they’re looking for, what price they pay, when they travel, what they like and don’t like. The hotel knows who’s sleeping in room 217 tonight, and not much else. Every interaction between guest and hotel is an isolated transaction. There’s no relationship. No memory. No context.

That’s what kills the hotel business in the medium term. Not the commission: the commoditization. If you don’t know your customer, you can’t retain them, you can’t anticipate their needs, you can’t offer differentiated value. If your only acquisition channel is the OTA, you depend on a channel controlled by someone else — one that tightens its grip every year.

And no feature, no matter how good, fixes that. The next wave of TravelTech won’t be won by whoever has the most technology. It will be won by whoever returns to hotels the control over their customer.

The real revolution isn’t selling more technology

It’s flipping the model. And that means three concrete things.

First: owned, unified data. A hotel needs a platform that brings together all guest information — bookings, preferences, interactions, behavior — in one place under their control. Not fragmented across five vendors. Not rented from an OTA. Owned.

Second: direct channels. Own website, own loyalty program, own campaigns. Not to “compete” with the OTAs, but to gradually reduce dependence on a channel hotels don’t control.

Third: continuous relationship. Every guest who walks through the door is an opportunity to start a relationship that doesn’t end when they leave. If the hotel knows who that person is, what they liked, what frustrated them, they can turn a one-time stay into a recurring customer. And a recurring customer is worth between 5 and 10 times more than a new booking acquired through a third party.

This isn’t a software change. It’s a mindset change. And that’s exactly why it’s so hard — and why so few companies actually scale.

And then AI arrives. And everything multiplies.

While this is playing out, the next wave is approaching: artificial intelligence. And most of the industry is looking in the wrong direction.

The public conversation about AI in hospitality is obsessed with models: which chatbot, which agent, which automation, which prediction. But models commoditize at brutal speed. GPT, Claude, Gemini, and whatever comes next. Within three years, any mid-budget hotel will have access to the same AI capability as Booking.

What doesn’t commoditize is the data.

If you have a PMS, a CRM, a loyalty system, and ten years of guest history — owned, unified, actionable — the AI you train on that data will be specific to your hotel, your market, your customer. It will be yours. It will be defensible.

If all of that is fragmented across your PMS, your channel manager, three OTAs, and half a dozen vendors that don’t talk to each other, you don’t have data to train on. You have noise.

And here’s the uncomfortable consequence: today, when a guest books through Booking, the relevant data from that booking feeds Booking’s AI — not yours. Every interaction enriches the OTA’s model: its ability to predict, recommend, retain, and sell. You just get a check-in notification.

In five years, OTAs won’t be intermediaries. They’ll be hospitality superintelligences trained on the data of the entire sector. And the hotels still operating in that model won’t be competing with a distribution channel — they’ll be competing with an AI that knows their customer better than they do.

The window to reclaim the data isn’t unlimited. The longer hoteliers wait, the more expensive and difficult it becomes. The next wave of TravelTech won’t be won by whoever has the best AI. It will be won by whoever controls the data that trains it.

This is what we’ve been building at Fideltour

Fideltour is one of the 10 tech scaleups in the Balearic Islands. One of the 24 TravelTech scaleups in all of Spain. We’ve spent years building exactly this: a hotel CDP and CRM platform designed so hotels stop renting their customer relationship to a third party — and reclaim it.

We don’t sell features. We sell a model. And the model is: the hotel that controls its data controls its future.

We operate from Mallorca, in the heart of what the data now suggests is Europe’s most efficient TravelTech hub. That’s not a coincidence. The Balearic Islands concentrate a unique density of hoteliers, operational know-how, capital, and technical talent. If the next wave of European TravelTech is going to come from somewhere, my bet is it’s coming from here.

The invitation

If you’re building in TravelTech: don’t launch another tool. Question the model. There’s room for you — but not in the feature war.

If you’re a hotelier: the most important question you’ll face in the next five years isn’t which software to buy. It’s who’s going to control the relationship with your customer — you, or a third party. You’re answering that question today, whether you realize it or not.

If you’re an investor: the data is clear. 24 TravelTech scaleups in Spain. 10 tech scaleups in the Balearic Islands. €454M invested in the sector last year. The curve has started.

The shift is already here. All that’s left to decide is which side you’re building from.

The Tech & Innovative Companies Report 2025 is available for download at https://elreferente.es/informe-empresas-tech-espana-2025/ Thanks to José María Torrego and the El Referente team for the rigor of the report.